|

Search | Back Issues | Author Index | Title Index | Contents |

![]()

D-Lib Magazine

|

|

|

James Currall |

![]()

IntroductionRecently we have seen a number of reports from the British Library in the UK1 and from the State library services in both Florida2 and South Carolina3 in the US, organisations that have started to develop ideas around measuring how much their work is worth to the communities they serve and thus to their paymasters.4 These cases highlight an interesting issue: how difficult it is to value that which is not tangible. Rather than focusing on a justification for funding, this paper will look at the issue of valuing intangibles within the context of digital preservation. Information and the values that it has are intangible. For information-rich organisations this means it is very hard to understand the benefits that the information brings and the results that investment can achieve. The espida project at the University of Glasgow, with funding from the Joint Information Systems Committee, is exploring how intangible assets might be valued in order to make a sound business case to ensure the longevity of information objects; in other words, achieve truly sustainable digital preservation. Most work that has described 'sustainable' digital preservation has assumed that the organisation in question will only ask, 'how much?' not, 'why?' The 'why' is the hardest question to answer, particularly when the objects being described are digital and the values derived from them are for the most part intangible. Decision-makers need to have very good reasons to divert resources from primary activities to digital preservation practices, and being able to answer 'why' is more than a matter of saying: 'because it is important'. TerminologyIt is necessary to briefly define some terms. We have mentioned 'information objects'. Simply, 'information objects' convey some sort of information or representation of knowledge. They can be in either digital or hard copy and are, in essence, objects created and/or used in everyday work environments. There is a large amount of literature that explains why, in the preceding sentences, the use of 'information' and 'knowledge' is problematic; however, the corpus on this area does offer us a description that is useful for our purpose. Buckland (1991) argues that there are three distinct meanings of information:

The first two are generally accepted as valid meanings of 'Information', but the third is more contentious, with a number of authors arguing strongly that 'Information as Thing' is not a valid meaning of information. Buckland argues that a manifestation/representation of information ('Information as Thing') is tangible, whilst knowledge itself can be represented in a tangible form (however poorly or incompletely) through 'Information as Thing'. Our purpose in drawing attention to Buckland's distinction is not to argue for or against his position. We are concerned with the preservation of 'Information as Knowledge', but preservation is more certain and controllable if there are representations of that information ('Information as Thing') as opposed to the information simply being in the minds of individuals. Throughout this piece 'Information as Thing' will be used interchangeably with 'information object' as, for us, it offers a valid description of what we believe information-rich organisations deal with. Digital Preservation and EconomicsThere is no need to regurgitate here what digital preservation is and why it is important; there are numerous places where digital preservation is defined and discussed, and we presume readers will already have a good understanding of the concepts and issues involved. It is becoming increasingly common within the literature, that 'softer' issues are more prominent. It would be churlish to suggest that the technical issues have been solved, but it is true that a stage has been reached where some technical solutions are deemed as viable, rather than seen only as abstract ideas. The main challenge at the moment is to ensure that organisations can retain assets into the long term. This goes far beyond solving the technological issue and even beyond the costing of digital preservation practices. It means convincing senior managers and decision makers of the value of their digital objects in order that the objects' retention is not only embedded in their strategic management rhetoric, but is also acted upon and given consistent and long-term resources. Carrying this out involves the use of some economic methodologies. However, it also asks a question that has rarely been asked in the literature, let alone answered: how do you communicate the value of information objects to decision-makers? Most authors work on the premise that the decision makers of their organisations understand exactly what assets they have and perceive the need for actions to preserve digital materials. This is often far from the case. Certainly, work has been and is being done on costing digital preservation.5 However, the methods employed do not take into account the actual assets that need to be preserved (managed), and it is generally assumed that the objects (with little communication of why they are 'assets') must be preserved. Business models must answer not only the question 'how much does it cost?', but also, 'why do we need this?' and 'why should we spend money on this, rather than on the primary business of the organisation?' These questions require very different answers than those that cost models can deliver. Brian Lavoie (Lavoie 2004 and Lavoie & Dempsey 2004) is one of the very few to properly explore preservation as an economic activity and look at making practices sustainable. He sees three things as key to this: responsibilities (which are split into areas); incentives (which need to be outlined for the decision-makers for the different areas of interest); and organisation (of preservation of objects). He rightly says that preservation is an investment and incentives must be made visible to decision makers in order that resources can be leveraged to preserve the objects (Lavoie 2004, 53). Incentives usually take the form of benefits to the organisation such as increased profit, but they can also take the form of intangible benefits such as increased kudos and reduction of risk. In the current climate, most organisations will only provide resources to ensure the longevity for those information objects that are assets. The crux of the matter is the definition of exactly what constitutes an asset to the particular organisation and then expressing that in terminology senior management can understand.6 The espida projectThe espida project at the University of Glasgow is exploring how intangible assets might be valued in order to make a sound business case to ensure the longevity of information objects. espida's work centres on a two-way dialogue with asset creators and senior management, and this dialogue has as its outcome a new understanding and way of thinking – a cultural shift. This means that these key players need to understand and be convinced of three things:

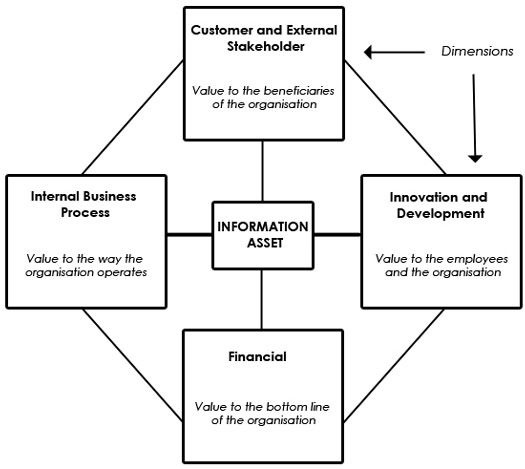

This engagement strategy also requires listening to and understanding object creators' perspectives on the value of objects and requirements for their retention. In many ways, the engagement strategy means that espida acts as an intermediary and translator between information creators and managers on one hand, and senior management on the other. While this work is being undertaken at the University of Glasgow, the methodology and tools created will be applicable to other Higher Education/Further Education (HE/FE) institutions and information-rich organisations. Indeed the remit for the project started as a business model for digital assets, but as will be seen below, it holds for other forms of assets as well. It is important to state that we are not selling 'digital preservation' to our senior management and asset creators, we are selling them the motivation to manage, reuse and preserve assets that are of value to them and the University. Information and ValuePlacing value on information is clearly very complex. It is not a simple matter to assess all the ways in which an organisation's information assets provide value to it, let alone discover ways of measuring how that value changes over time. Our focus is on the entire panoply of information assets, published, unpublished, raw or processed, that characterise an information-rich enterprise. The value of these assets is often hidden or simply assumed to be there, for example, the minutes of Senior Management meetings are assumed to be valuable to the University, but not all of the areas of value they have are known or understood.7 We wish to express the value of these assets in clear business terms whilst not reducing everything to a purely financial expression. A Model of ValueWe propose a robust model of value to an organisation of its information objects, in four principle dimensions summarised in Diagram 1. Some might recognise these dimensions as having more than a passing similarity to the Balanced Scorecard (BSC) of Kaplan and Norton, used as a tool in business planning and performance (Kaplan & Norton 1992, 2001). This is no coincidence. In defining value, we are seeking to move the discussion of digital preservation to the domain of decision makers (at whom Kaplan and Norton target their ideas). Our adaptation of the BSC does not put processes or the organisation in the middle of the card, but rather information objects, in order to utilise the four dimensions of the scorecard to explore perspectives of value. The elements of value within the dimensions are ones to which 'Information as Thing' creators can relate. The four dimensions force a detailed analysis of what value information objects bring to the customers and external stakeholders, how the objects benefit the advancement of employees (including their well-being and personal development), what value the object brings to the workings of the organisation (in particular efficiency and effectiveness) and finally, the financial value through cost saving or income that the object can bring.

Each dimension has many different elements, and understanding value as a whole requires identification of all these elements. This is done with the help of the object creators and information professionals. Some common areas of value are the quality of teaching and research, compliance with legislation and the accessibility of resources. Different departments within the University have some unique areas of value as a result of the nature of their work, and these prove to be excellent material in relation to building a business case.8 The reason we chose to adapt the Balanced Scorecard (BSC) is evident within its name. The BSC not only allows the business case developers to fully explore all areas of value, it also presents the multiple dimensions of value to the decision-makers. They no longer only see financial figures of cost income; they also see other, more intangible values. The dimensions and elements through which value is explored are tied strongly to the organisation's strategy and goals. Not all of the areas discovered in our discussions with object creators and information professionals have had relevance to the strategy and are therefore not included, as they are not of strategic benefit to the organisation. A breakdown of the BSC dimensions into its elements is given in Appendix 1. Note should be made of two things. Firstly, the elements in our BSC are directly related to the University of Glasgow's strategic plan (a research-led institution). To be of use to other organisations these elements will likely have to be modified to reflect the strategic goals of those organisations. Secondly, throughout our work it has become apparent that this methodology allows the expression of value of many forms of objects, not just those in digital form. We would propose, therefore, that this adaptation of the BSC is of relevance to a great range of organisations that need to communicate or understand the value of their assets. Value MetricsHaving established the components of value that are important, we need to be able to produce suitable metrics for them. These metrics must be:

These metrics do not have to be:

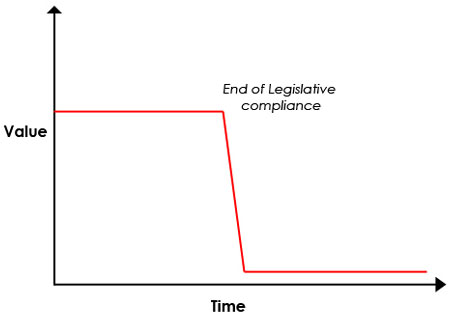

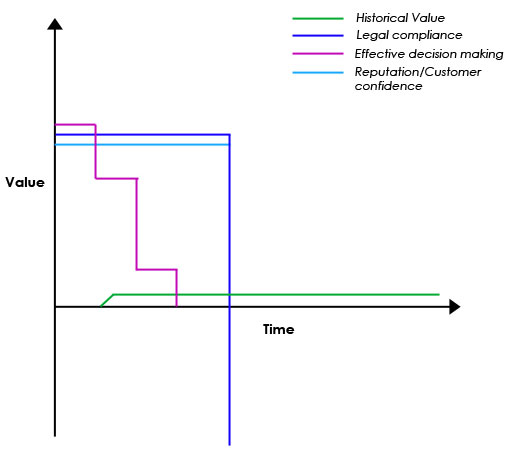

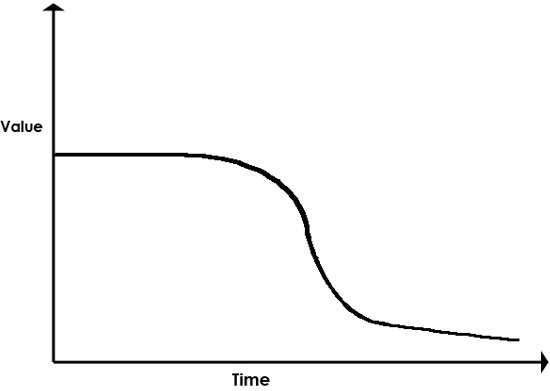

Problematically, value is a concept that is not absolute and therefore demands flexibility. How exactly do you measure the value that a digital asset brings to the Intellectual Capital within the University? (Number of academic papers? Research rating? Financial value of grants and contracts?) This area is the focus of our work over the next few months. Value over timeValue is not constant. It does not remain static, nor indeed does it keep the same dimensions and elements. This property of value means that the model must explore what happens to the value of different asset types as time passes. The process of defining value allows organisations to appreciate proper management of the assets, which includes timely destruction of those assets when their value reaches a point where it is no longer of benefit to retain them (or indeed, too risky). Graph 1 displays a value/time graph for financial records. Initially the records are of high value – coming from the efficiency of operation and effectiveness of decision-making. However, the key value is that of complying with legislation. Once the legislative requirements are no longer in force then the value drops to almost zero (historical value only remaining). Historical value can be found for almost any information object and is itself composed of different value dimensions, but this is often not a value that sits with the strategic aim of the organisation, and therefore not a relevant one.9 There are more things happening in the graph other than this 'top-line' of value. Graph 2 attempts to display how all the elements of value act over time. It shows that the high value in the beginning of Graph 1 is composed of other elements of value (predominantly those of effective decision making, reputation and customer confidence). It also details that at the end of the legislative period the immediate effect is one of negative value: keeping the record exposes the organisation to risk. The end of the compliance period is so destructive to the value of the asset because the only other area of value acting on the object at that point in time is that of historical value. Graph 1 may be a simplified version of Graph 2, but it takes account of all the values and events that act on the object.

These two graphs show that value is multifaceted and changes over time. Different values have different impacts throughout the lifetime of the asset. Appendix 2 details further value/time graphs for different asset types, some of which show that value can rise as well as fall. ConclusionsDigital preservation is an investment decision, where expenditure in the current period is made in the belief that benefits will accrue in some future period and, as such, needs to have the benefits weighed against the costs and risks. Viewed in this light there must be, in some sense, a return on that investment. What we are doing in espida is looking very carefully at the nature of that return and being very clear that the return (or benefits) may take forms other than the directly financial. This paper has focussed on value as a strong driver for action and has only mentioned in passing the concept of risk. It should not be inferred that risk does not play a large role in espida's work. The business case that will be made will closely examine the role of risk, as it is one of the three legs of the stool on which the business-case rests (value, cost, risk). Why this should be of interest to me?The process of valuing information is complex. Our work has shown that there are many different dimensions of value and people have different perspectives on those dimensions. The task that espida is undertaking will be of relevance to people who need to be able to understand or communicate the value of information objects. This ability to communicate unlocks a number of doors: information creators will be able to rationalise expenditure on representations of intangible assets far more readily; and the methodology can be used to make lucid and strong business cases to decision makers about intangible objects and values. The model we have created was produced to argue a case for sustainable resources to ensure the longevity of digital assets. For this purpose it works well. It is also the case, however, that our work holds potential for other stakeholder communities, not just information professionals worried about digital obsolescence. Technology providers could use it to define contexts for their innovations in technology, and organisations could use it to give creators clearer ways of assessing the value of their efforts. Better stewardship of information assets will also be an outcome of any discussion on value. This may result in either the destruction of objects, or ensuring their longevity and the widening of access and use to reap the full value of them – once the investment has been made the return might exceed even the most optimistic business case.Appendix 1: The espida Balanced Scorecard

Appendix 2: Value/Time Graphs for Information Objects

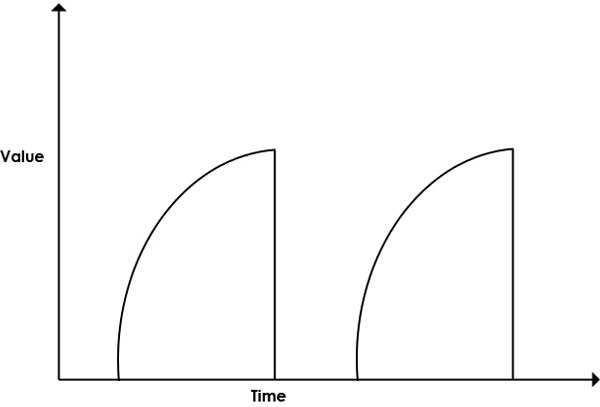

These resources are brought in from external sources. There are strict rules in terms of number of users. The value of the resource increases to a peak just before the class examination, then it falls to zero. The resources are brought in every new academic year.

Committee documents include agendas, minutes and reports and papers used during committee business. While they are current, their value is high. This value drops off as they fall out of use and relevance. The value of the resource depends on reliability and functionality. The ease of use will widen the audience. The value declines to historical value. Of course it is perhaps the case that the historical value of these documents may be higher than that of other information objects.

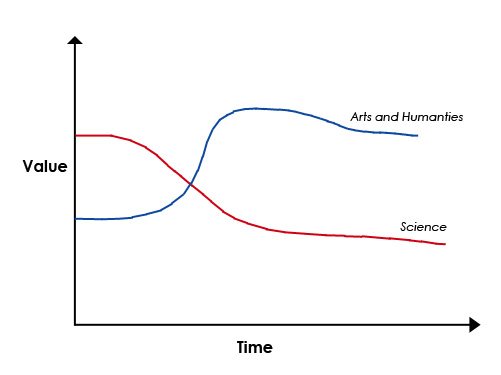

The shape of value is very much dependant on the subject discipline that the work was done under. Science theses start with a high value, which comes mainly from the freshness of the research to the community, but this begins to decay quite early on as the research is superseded in the fast moving scientific field. However, in the Arts and Humanities field, the value is not initially as high, but climbs as more people become aware of the new research. It is a slower moving field than that of the sciences, thus the value is held for longer. The value of Humanities theses will always remain higher than those from a Science background. Interestingly,the shape would remain unchanged if it were redrawn for hard copy theses. Notes1. The BL study Measuring our Value is available at: <http://www.bl.uk/pdf/measuring.pdf>. 2. The Florida study report is available at: <http://dlis.dos.state.fl.us/bld/roi/index.cfm>. 3. The South Carolina study report is available at: <http://www.libsci.sc.edu/SCEIS/home.htm>. 4. The method used by the libraries is that of contingent valuation. Very simply this uses questionnaires and other tools to ask 'how much would you pay to use this service if it was not there?' For further examples of this method see Duberstein & Steiguer (2003) and Arrow et al. (1993). 5. Most work has looked at the elements of cost that must be accounted for (ERPANET 2003; Russell & Weinberger 2000; Hendley 1998), with little practical examples of actual costs. Many have signalled that the complexity of singling out costs of preservation from other costs such as creation and management clouds the issue, but this is perhaps a complexity that is false: all the costs are relevant to the longevity of digital materials. Oltmans has compared the cost implications of choosing one method of preservation over another (emulation and migration) and finds that the cost pattern differs, (Oltmans & Kol 2005). Work is being done in great detail at the Cornell Institute (see most recently Kenney 2005). 6. There is of course the question of potentiality. The information objects may become assets in the future. This is the concept that companies use when paying for the upkeep of their patents. The vast majority of them will not be valuable in the future, but one or two could make the investment worthwhile. 7. Our work so far has discovered that while the act of recording the meeting is of value to the committee for its work, the overall value to University (communication and accountability) is far from being recognised by the committee. 8. For example, one of the Faculties within the University has commercialised technologies it has developed. 9. This is certainly true of most of the assets within the particular organisation we are dealing with. However, memory organisations deal in historical value, and could use our methodology to help them explore the different elements of historical value to aid them in selection and appraisal. For more on this see Currall, Johnson & McKinney (2005). BibliographyArrow, Solow, Portney, Leamer, Radner, and Schuman. 1993. Report of the NOAA Panel on Contingent Valuation. In Federal Register. Washington D.C. 58. Buckland, Michael. 1991. Information as Thing. Journal of the American Society for Information Science, 42 (5):351-360. Currall, James, Claire Johnson, and Peter McKinney. 2005. 'The Organ Grinder and the Monkey. Making a business case for sustainable digital preservation', given at EU DLM Forum Conference 5-7 October 2005 Budapest, Hungary. <https://dspace.gla.ac.uk/handle/1905/455>. Duberstein, Jennifer N., and J.E. de Steiguer. 2003. Contingent Valuation and Watershed Management: A Review of Past Uses and Possible Future Applications. In First Interagency Conference on Research in the Watersheds: U.S. Department of Agriculture, Agricultural Research Service. ERPANET. 2003. Cost Orientation Tool, <http://www.erpanet.org/guidance/docs/ERPANETCostingTool.pdf>. Hendley, Tony. 1998. Comparison of Methods and Costs of Digital Preservation. In A JISC/NPO Study within the Electronic Libraries (eLib) Programme on the Preservation of Electronic Materials. Kaplan, Robert S., and David P. Norton. 1992. The balanced scorecard - measures that drive performance. Harvard Business Review 70:58-63. Kaplan, Robert S., and David P. Norton. 2001. The Strategy-Focused Organization. How balanced scorecard companies thrive in the new business environment. Boston: Harvard Business School. Kenney, Anne R. 2005. The Cornell Experience: ArXive.org. In DPC/DCC Workshop on Cost Models for Preserving Digital Assets. British Library. <http://www.dpconline.org/docs/events/050726kenney.pdf>. Lavoie, Brian F. 2004. Of Mice and Memory: Economically Sustainable Preservation for the Twenty-first Century. In Access in the Future Tense. Washington, D.C.: Council on Library and Information Resources. Lavoie, Brian, and Lorcan Dempsey. 2004. Thirteen ways of looking at: digital preservation. D-Lib Magazine 10 (7/8). <doi:10.1045/july2004-lavoie>. Oltmans, Erik, and Nanda Kol,. 2005. A Comparison Between Migration and Emulation in Terms of Costs, RLG DigiNews, 9 (2) April 15. <http://www.rlg.org/en/page.php?Page_ID=20571>. Russell, Kelly, and Ellis Weinberger. 2000. Cost Elements of Digital Preservation. <http://www.leeds.ac.uk/cedars/documents/CIW01r.html>. (On April 19, 2005, at the authors' request this article was corrected to include a reference to work by Anne Kenney.) Copyright © 2006 James Currall and Peter McKinney |

|||||||||

| |

|||||||||

|

Top | Contents | |||||||||

| | |||||||||

|

D-Lib Magazine Access Terms and Conditions doi:10.1045/april2006-mckinney

|